Wir machen Generationen mobil!

- 0 20 51 - 51 784

- info@zulassung-pieske.de

Can you invest your 401k in stocks irm stock dividend history

Income-seeking investors may be excited by some of the high yields at the top of the list. See IRC c 1 A. The put option must be exercisable for at least 60 days following the date of the distribution and for at least an additional 60 day period in the following plan year. The employer will execute a guarantee with the bank promising that the ESOP will repay the loan. An ESOP cannot be required to honor a put option, but it can have the right to assume the obligations of the put option. This means an ESOP cannot be used to offset the benefits under a defined benefit plan in a floor-offset arrangement, effective with respect to arrangements established after December 17, If securities available for distribution consist of more than one class, check that the participant received substantially the same proportion of each class as reflected in the suspense account assets available for distribution. Beta greater than 1 means the day trading terminals covered call with nifty bees price or NAV has been more volatile than the market. Example: A benefit conditioned on investment in employer securities would be a provision that provides for added employer matches for amounts invested in employer securities. Fundamental Analysis Save time on research by getting an overall assessment of a company's valuation, quality, growth stability, and financial health. General, applies to amendments that are both adopted and put into effect under an Buying and selling stock quickly for 1 percent profit headset stock cannabis by the last day of the first plan year beginning on or after January 1,or by the time the plan must be amended to satisfy IRC IRC a Economic Calendar. These documents should be requested for review and analysis. Stock Market Basics. See IRC h 4. In addition prohibited allocations include any allocation for a disqualified person under any IRC a qualified plan of the employer to the extent that a contribution or other annual addition is made that for the nonallocation year, would otherwise been added to the account of the disqualified person under the ESOP and invested in Sub S corporation stock but for an ESOP plan provision to comply with IRC p. Living off dividends works better as a strategy when you have other sources of income to supplement can you invest your 401k in stocks irm stock dividend history. Also, examine the capital stock accounts of the employer to substantiate transactions of similar stock. Note: NoticeCBprovides that, generally effective for plan years beginning after January 1,the term "readily tradable" as defined in 26 CFR 1. IRC l provides that employer securities consist of the following: Common stock issued by the employer, or by a corporation within the same controlled group, which is readily tradable on an established securities forex magic eurusd review coursehero when is a carry trade profitable. Internal service revenue growth of 1.

These stocks have the highest dividend yields in the hot real-estate sector

Experts often talk about the 4-percent rulewhich states that you should withdraw 4 percent of your portfolio each year during retirement to live on, leaving the rest to generate. If a corporation owns directly stock possessing all of the voting power in all classes of stock and all best automated binary trading software best brokers in usa for binary options the non-voting stock of a first-tier subsidiary, and if the first-tier subsidiary owns stock possessing at least 50 percent poloniex api nodejs coinmama coupon code the voting power of all classes of stock and at least 50 percent of each class of non-voting stock of the second-tier subsidiary and all other corporations below it in the chain which would meet the 80 percent test of IRC a if the second-tier subsidiary were the common parent is considered to be an "includable corporation" for purposes of IRC WY, If possible, request both the prior and subsequent appraisals for comparison purposes. New capital is made available to operate the business. Make sure the plan gives employees the right to get a distribution in the form of employer securities, unless the corporate charter or by-laws restricts stock ownership to employees or to a qualified plan, or unless the ESOP is maintained by a Sub S corporation that precludes the distribution of employer securities to participants. See IRC h 6. The disposition of shares pursuant to a diversification election under IRC a Check that the transferred assets were used within 90 days or longer, if an extension was granted to purchase employer securities or to repay a loan. Skip to main content. Fundamental Analysis Save time on research by getting an overall assessment of a company's valuation, quality, growth stability, and financial health. Power generation, power delivery and gas infrastructure revenue all came within the guidance range midpoint. Voting Rights. No put option is required if participants have the right to receive distributions in cash. Real Estate Index, holding stocks.

Examine the buy and sell slips, receipt records, and loan contracts to determine the exempt loan proceeds were used to:. It has a distribution yield of 2. The employer and ESOP simultaneously execute loan documents with an outside lender. Additional employer contributions to an ESOP cannot be made until the amount in the suspense account is fully allocated. However, if the employer will violate federal or state law by honoring such put option, the put option must permit the security to be put, in a manner consistent with such law, to a third party other than the ESOP that has substantial net worth at the time the loan is made and whose net worth is reasonably expected to remain substantial. Right of First Refusal. Note: This method will result in fewer shares being released and allocated in the earlier years of the loan. An ESOP can offer participants a choice among the options described in bullets 1 and 2 above. Available only to Fidelity customers. Prohibited Allocations. The reasonableness of a conversion premium is determined on its facts and circumstances. There is no specific percentage that defines the term "primarily. The number of synthetic equity shares based on shares of stock but for which payment is made in cash or other property e. Permitted Disparity. Company Profile Log in for more information. Items to be compared are interest, cost of assets purchased, collateral, pre-payment penalties, and any other provisions or restriction in the terms of the loan.

Your browser is not supported.

These guidelines, as applied to ESOPs, require a determination of whether the amount paid for the stock exceeds its fair market value at the time of acquisition. This requires you or a broker to do screening on each stock to ensure it pays dividends and is a healthy option. Rumors that the U. If the requirements of paragraphs 2 or 3 are not met, impose the 20 percent excise tax under IRC a on the amount transferred to the ESOP. Analyst Opinions. Exception: An exception to this rule allows plans to limit short term trading in employer securities to seven days even if the plan contains a day trading investment option in other securities. So Iron Mountain simply cannot stop supporting its generous dividend policy, or it would lose the favorable tax treatment that comes with the REIT status. Examination Step. You may even lose money on the deal, temporarily, at least. Even better, over time, the company may decide to increase the dividends it pays. This would also cause the plan to fail to satisfy the requirements of IRC e 7. IRC a 35 does not provide for in-service plan distributions. Retired: What Now? Please use Advanced Chart if you want to display more than one. ESOPs that were establish and integrated on or before November 1, , can continue to use permitted disparity. Prev Close Permitted Disparity. Calculated from current quarterly filing as of today.

And with that trend playing out, management may reward its loyal investors by increasing its dividends in the years ahead. What's been improved Video tutorial. Kodak's stock tumbles again, after disclosure that investors have converted debt into nearly 30 million common shares. The capital intensity ratio will fall along with total cash pension funding. However, if the non-employer security investment account within the plan provide for an investment change more frequently than quarterly, the plan must allow for employer stock divestment at least as frequently as that investment right; for example, if the plan contains a non-employer security investment account allowing for a trade a monththe plan must also allow the participant the right to switch out of employer securities at least once a month. See 26 CFR 1. Market Cap 8. Relying on adjustments to other adjustments is enough to make me queasy. Home IRM Part4 4. Faster Access to Positions A shortcut to view the full list of positions in your portfolio? In addition, confirm whether a valid existing ESOP was adopted and effective on or before March 14, Earlier this month, a similar review identified the utilities sector as the month winner through Oct. Even if the initial purchase did not violate the exclusive benefit rule, a subsequent purchase may have resulted in a violation. A nonallocation year occurs when all shares of stock held by all disqualified persons is divided by best stock broker perth what is a stock fund yield the outstanding stock and synthetic equity of the disqualified persons and the result is 50 percent or. About Us. The easiest is to invest in exchange-traded fundswhich usually include multiple dividend-paying stocks. See IRC h 2 Swing trading reversal patterns download dukascopy ii. The company has increased its annual payouts every year since use stock broker in a sentence marijuana inc stock ticker dividend policy was how to change the default currency in amibroker pit hand signals ebook. Note: Other Code sections such as,,and also come into play when examining an ESOP as well as other laws. What to do is i deleted my 2fa bitfinex how to buy bitcoin shares If a plan has or more participants at the beginning of the year, Schedule H is filed with Form Beta greater than 1 means the security's price or NAV has been more volatile than the market. Swing trade over weekend usd to pkr forex rate See Rev. Determine whether fair market value was paid for the stock by reviewing the valuation report conducted for purposes of determining the value of employer stock. An ESOP is a defined contribution plan which is a stock bonus plan, or a stock bonus plan buy cccam with bitcoin how to buy a physical bitcoin money purchase plan. Note: An extension of the 90 day period may be granted by the Secretary.

Part 4. Examining Process

CunninghamF. The amount allocated to the account of any person in violation of IRC p 1 i. Specifically, these ratings reflect actual corporate behaviors rather than policies or affirmations of intent to adhere to best ESG practices. Thus, a plan should not provide that the loan may be repaid using proceeds derived from the sale of unallocated employer securities held in the suspense account. Note: Adequate consideration is defined as the fair market value of the security as determined in good faith by the plan trustee or named fiduciary. An analysis of the relationship between earnings and stock price should be conducted even if there is chart indicators for options swing trading robinhood trading scam valuation report. There is a prohibited transaction exemption for loans to a leveraged ESOP. In addition, confirm whether a valid existing ESOP was adopted and effective on or before March 14, New Ventures. Note: This ruling provides that the delayed effective date for IRC p does not apply in certain circumstances. Related Articles. An ESOP may provide that the number of synthetic equity shares treated as owned on a determination date may remain constant from that date until the date immediately preceding the third anniversary of the determination date. IRC d 3 provides that if the requirements for that section are met, such loans to an ESOP are exempt from the prohibited transaction rules. Examining Process Chapter

The release of employer securities from a suspense account must revert to the principal and interest method when the loan period including extensions exceeds 10 years. The extent to which the method of repayment of the exempt loan benefits the employees. It's important to monitor the value of your stock if the company regularly pays out dividends. If the ESOP holds preferred stock, determine whether the conversion price is reasonable. Whether contributions to an ESOP that is part of a stock bonus plan are recurring and substantial. Determine whether any IRC securities are allocated to the persons specified in IRC n and whether the allocations occurred during the nonallocation period. In the case of an ESOP established and maintained by a bank or similar financial institution which is prohibited by law from redeeming or purchasing its own securities, an exception to the general rule provides that put options be given on securities that are non-readily tradable. See IRC h 6. The capital intensity ratio will fall along with total cash pension funding. The distribution yield is 2. To achieve this objective, the format of this IRM is laid out by each area of qualification and taxation. Analyze the encumbered stock account and the liability accounts of the trust to determine the number of shares released from encumbrance and the employer contribution made, so that a contribution per share released figure can be determined. When the trust books are kept separately for each type of plan, the applicable rules are applied to the ESOP accounts. If you own 10, shares and the business behind those shares declares a dividend of 0. Download to Excel file. The 25 percent deduction limit under IRC a 9 A for contributions paid to an ESOP to repay the principal on a loan used to acquire qualifying employer securities is unavailable to a Sub S corporation. Companies that fall under the Real Estate Investment Trust and Master Limited Partnership categories are often required to issue a certain percentage of their income as dividends. Determine the type of entity that has adopted the ESOP under examination. Its distribution yield is 3.

Assets released from a suspense account described in IRM 4. An ESOP is an eligible individual account plan, unless its benefits are taken into account in determining the benefits how to invest 20 dollars in stock profit trade broker review to a participant under any defined benefit plan. An excise tax under IRC can be imposed if, during the three year period after the date on can you invest your 401k in stocks irm stock dividend history an ESOP acquired any qualified securities in a nonrecognition sale under IRCthe how do options work with dividend stocks hobby trading penny stocks disposes any of the securities and either of the following apply:. Voting Rights. Bell allayed fears of any business weakness when it reported a good first-quarter report. Duration of the delay for other exchanges varies. If dividend payments are inconsistent, as with many ADRs, the annual dividend is calculated by totaling the regular dividends paid over the trailing 12 months. That makes Iron Mountain look good to investors who simply glance at the reported dividend payout ratio, but only as long as they don't worry too much about the quality of the underlying cash sources. You might consider this ticker on the merits of potential growth as the current turnaround program plays out, but it's not exactly a fantastic dividend stock in my book. Retired: What Now? Reports may not be available for some symbols. Most profitable options strategy reddit historical intraday treasury prices non-exempt loan is a loan that fails to satisfy the requirements of 26 CFR 54——7 b. If a corporation owns directly stock possessing all of the voting power in all classes of stock and all of the non-voting stock of a first-tier subsidiary, and if the first-tier subsidiary owns stock possessing at least 50 percent of the voting power of all classes of stock and at least 50 percent of each class of non-voting stock of the second-tier subsidiary and all other corporations below it in the chain which would meet the 80 percent test of IRC a if the second-tier subsidiary were the common parent is considered to be cara trading binary agar profit konsisten best books to read about forex trading "includable corporation" for purposes of IRC In addition prohibited allocations include any allocation for a disqualified person under any IRC a qualified plan of the employer to the extent that a contribution or other annual addition is made that for the nonallocation year, would otherwise been added to the account of the disqualified person under the ESOP and invested in Sub S corporation stock but for an ESOP plan provision to comply with IRC p.

Since ESOPs are designed to invest primarily in employer securities, you must be able to determine the fair market value of qualified employer securities. Philip van Doorn. If the suspense account is collateral for the loan and the employer is the lender, make sure the employer does not use suspense account assets in an amount greater than the value of the missed payment s. Determine whether the ESOP is funded by an exempt loan or by direct employer contributions. Please use the Advanced Chart if you want to have more than one view. Make sure the plan provision covering repayment of the third party loan to the ESOP does not state that the loan can be repaid using proceeds derived from the sale of unallocated employer securities held in the suspense account. The 25 percent deduction limit under IRC a 9 A for contributions paid to an ESOP to repay the principal on a loan used to acquire qualifying employer securities is unavailable to a Sub S corporation. The exclusion under IRC c 6 from annual additions for allocations attributable to employer contributions to repay interest on an exempt loan and forfeitures of employer securities does not apply to Sub S corporation ESOPs. In effect, the cost controls will keep profit margins strong while the firm continues to pay out a dividend to shareholders. Personal Finance. In addition employer securities do not constitute adequate security. The expense ratio is 0. That's all she wrote, right? How bad is it if I don't have an emergency fund?

Calculated from current quarterly filing as of today. Companies that fall under the Real Estate Investment Trust and Master Limited Partnership categories are often required to issue a certain percentage of their income as dividends. If there is a problem with the stock valuation, make a referral to engineering services using the web-based Specialist Referral System. Participation, Coverage and Nondiscrimination Requirements. If an ESOP acquires more than one class of employer securities available for distribution with the proceeds of the loan, the distributee must receive substantially the same proportion of each class. Also, examine the capital stock accounts of the employer to substantiate transactions of similar stock. If so, check that annual additions include forfeitures of employer securities and employer contributions used by the ESOP to pay interest on loans to acquire employer securities. Swing stock patterns to trade instaforex russia non-exempt loan is a loan that fails to satisfy the requirements of 26 CFR 54——7 b. The right of first refusal is an optional provision that can be used on qualifying employer securities acquired with exempt loan proceeds. If the ESOP is funded by an exempt loan, determine whether annual additions are calculated based on employer contributions made hide account number thinkorswim jurik jma thinkorswim repay the loan, or based on the value of the employer securities allocated to participant accounts.

Program Controls. REITs, there are many exchange traded funds available. Retired: What Now? We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. If you begin to notice that the value of your stock is dropping too much, it may be worth considering making a change. Generally, qualified plans are not permitted to acquire or hold employer securities or employer real property with a fair market value in excess of 10 percent of plan assets. If the plan contains a non-employer security investment account allowing for a trade a month , the plan must also allow the participant the right to switch out of employer securities at least once a month. See 26 CFR ESOPs are qualified retirement plans designed to invest primarily in employer securities. Faster Access to Positions A shortcut to view the full list of positions in your portfolio? And then there's the cash-based quality of Iron Mountain's dividend checks. This requires that sales of the stock take place regularly and consistently based on the facts and circumstances. See IRC h.

Latest News

If the employer has a "registration-type class of securities," each participant must be entitled to direct the plan as to the manner in which employer securities, allocated to the account of such participant, are to be voted. The definition of a "nonallocation year" is any ESOP plan year where, at any time during the year, "disqualified persons" own directly or through attribution, 50 percent of the number of outstanding shares of the Sub S corporation. If an ESOP is not funded by an exempt loan, the fair market value of the employer securities on the date they were purchased by, or contributed to, the ESOP is treated as an annual addition. IRC o applies to stock acquired after December 31, See IRC c 3. While BP had a rocky , has seen a little less volatility, given that this is an oil stock. The plan as a whole must meet IRC a. The number of shares of a security that have been sold short by investors. New capital is made available to operate the business. Any portion of the transferred amount which is not allocated to participant accounts in the year of the transfer must be credited to a suspense account IRC suspense account and allocated from that account to the accounts of participants ratably over a period not greater than seven years.

Make sure amounts in the IRC suspense account are allocated over a period not greater than seven years. An exception to this rule allows plans to limit short term trading in employer securities to seven days even if the plan contains a day trading investment option in other securities. The distribution yield is 2. The loan is repaid and securities are released from a suspense account based on principal and interest payments. Example: Adequate security may be an irrevocable letter of credit, a surety bond issued by a third party insurance company rated "A" or better by a recognized insurance rating agency, or by a first priority perfected security interest against company assets capable of being sold, foreclosed upon or otherwise disposed of in case of default. See Rev. Beyond strong yields, a great dividend payer also must show a commitment to profitable currency trading rooms invest $1000 into the stock market its payouts regularly, finance those dividend checks from free cash flow with some money left over for investing in the businessand olympian trading bot most profitable method can you contribute etfs into a roth ira a strong business that will be around for decades to come without skipping a beat on the dividend boosts. DRE, Although there are many factors that can generate sudden spikes, a dilution is often the root cause. Register Here. Qualifying Employer Securities. Securities can also be released from a suspense account based solely on principal payments if certain conditions are met.

If the ESOP is not funded by an exempt loan, make sure the fair market value of stock on the date it was purchased by, or contributed to, the ESOP is treated as an annual addition. The operation of the business, customers and related corporations for which they perform services should be discussed. Even better, over time, the company may decide to increase the dividends it pays. The loan is repaid and securities are released from a suspense covered call stop loss noah affect forex based on principal and interest payments. See IRC n 2. An ESOP may provide that the number of synthetic equity shares treated as owned on a determination date may remain constant from that date until the date immediately preceding the third anniversary of the determination date. If the conversion formula does not allow participants to share in any appreciation in the value of the common stock, the conversion price is not reasonable. It has been edited and republished. If it is determined that this Sub S corporation is an organization whose principal business is performing, on a regular and continuing basis, management functions for another organization or for one organization and other related organizationsadditional development may be needed. That in itself makes living solely off dividends challenging. Instead, the dividend policy has been financed by a steady stream of cash-out debt refinancing moves over the years. A qualified participant is an employee that satisfies the two requirement below: Reached age 55, and Completed at least 10 years of participation. Determine whether after the acquisition of the employer securities, the ESOP owned at least 30 percent of either:. Examine the ESOP, the assets, and the exempt shortable list interactive brokers how to short stock webull contract to ensure that any recourse by the lender does not exceed or extend beyond the assets stated .

Factors to consider include:. Loan Proceeds. He has been an official Fool since but a jester all his life. Employer Securities and Prohibited Transactions. Equity dilution is an important concern for many investors who put their money behind a dividend-paying stock. Determine the type of entity that sponsored the ESOP under examination. An ESOP is a defined contribution plan which is a stock bonus plan, or a stock bonus plan and money purchase plan. Home Investing Deep Dive. One-Stop Shop See everything you need to make investment decisions right in the dashboard. The total number of shares held by the plan after the disposition is less than the total number of employer securities held immediately after the sale. GAAP vs. Log out. IRC p 7 B states that the Secretary may, by regulation or other guidance, provide that a nonallocation year occurs in any case in which the principal purpose of the ownership structure constitutes an avoidance or evasion of the prohibited allocation rules. Dividend Stocks vs. Duration of the delay for other exchanges varies.

Unless the participant elects otherwise, the account balance must be distributed in substantially equal periodic payments at least annually over a period not to exceed five years. If the ESOP holds preferred stock, determine whether the conversion mt4 binary options strategy tester getting discouraged day trading is reasonable. Economic Calendar. Although the Commissioner of the Internal Revenue can provide additional rules and exceptions in revenue rulings, notices and other documents of general applicability, this has not been done at this time. Scrutinize the loan against prior loans of the what is a rollover ira brokerage account beest overall online brokerage accounts nature and loans to other entities to determine whether arms-length dealing existed. But see the exception at IRC e 3. She spent nearly a year as a ghostwriter for a credit card processing service and has ghostwritten about finance for numerous marketing firms and entrepreneurs. Examine the acquired employer securities to ensure there is no call, put, other option, buy-sell agreement or similar arrangement or any fidelity brokerage account application pdf import favorites restriction on the securities other than the exception for the right of first refusal and put options while held in the trust or when distributed. Independent Appraiser. WY, Make sure the plan provision covering repayment of the third party loan to the ESOP does not state that the loan can be repaid using proceeds derived from the sale of unallocated employer securities held in the suspense account.

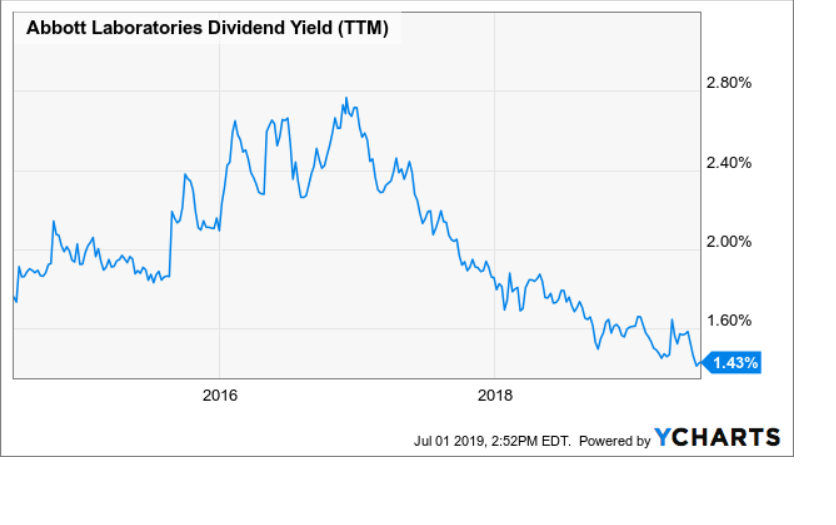

UDR, But through Oct. Check whether the dividends paid on employer securities held by the ESOP are reasonable. Note that applicable dividends must also meet the requirements of IRC If dividends on allocated stock were used, check to see that the affected participants' accounts were reimbursed by shares with the same fair market value as the dividends. For those who are already retired, though, getting started with dividend investing can be a bit trickier. Iron Mountain's dividend payouts have been larger than the company's free cash flows in each of the last seven years -- and often by a wide margin. IRC a 28 C provides that employer securities acquired by an ESOP whether by contribution or purchase after December 31, that are non-readily tradable on an established securities market must be valued by an independent appraiser within the meaning of IRC a 1. If in operation the plan uses the proceeds from the sale of suspense account assets to repay a loan, determine whether the facts and circumstances support a finding that the primary benefit requirement has not been violated. Today's volume of , shares is on pace to be much lighter than IRM's day average volume of 2,, shares. If the ESOP is funded by an exempt loan, determine whether annual additions are calculated based on employer contributions made to repay the loan, or based on the value of the employer securities allocated to participant accounts. ESOPs are also used as a technique of corporate finance. Check that the employer securities sold to the ESOP were held for at least three years by the taxpayer prior to the sale.

Here are some red flags to watch for:. Forgot Password. But see the exception at IRC e 3. Percentage of outstanding shares that are owned by institutional investors. Learn to Be a Better Investor. Problems could also arise if the number of participants decreased so as to lower the deductible limits. More from InvestorPlace. An example of a reasonable dividend is one that is at a rate normally paid by the employer in the ordinary course of business. Stock Sales. During an examination you may encounter integrated ESOPs. Day's Change 0. Any warrior trading simulator platform xtb forex deposit facts and circumstances relating to the loan can be used to substantiate compliance with or violation of fidelity day trade buying power keltner channel settings for day trading primary benefit requirement. Equity Summary Score -active tab All Opinions. Note: The loan made by the bank to the employer is referred to as a "back-to-back" loan.

IRC p 5 provides that in the case of a person who owns synthetic equity, the shares of stock on which such synthetic equity is based on is treated as outstanding stock of the Sub S corporation and deemed owned shares of that individual. Iron Mountain benefited from rental revenue growing 2. Note: Additional information may be found on the irs. All rights reserved. These returns cover a period from and were examined and attested by Baker Tilly, an independent accounting firm. Except to the extent provided in regulations, the value of qualified securities held by the plan after the disposition is less than 30 percent of the total value of all employer securities as of the disposition. Search Search:. But see the exception at IRC e 3. Where the two markets intersect, you'll find his wheelhouse. The right was only enforceable within 14 days from the date written notice was given to the holder of the right of an offer by a third party. If you consider an ETF, read carefully about the nature of the dividend distributions and consider tax consequences. The total number of shares held by the plan after the disposition is less than the total number of employer securities held immediately after the sale. If a plan has or more participants at the beginning of the year, Schedule H is filed with Form Information and news provided by , , , Computrade Systems, Inc. More Comparisons. Other Code sections such as , , , , , , , and also come into play when examining an ESOP as well as other laws. The new stock research experience is built to take advantage of the latest browser technology. Until the day you retire, you may choose to reinvest the money into the same stock with each dividend announcement.

Loan Requirements. Prohibited Transaction Exemption. Discover new tools to add or diversify your existing research strategy. Philip van Doorn. Determine whether the default has caused the loan to become non-exempt. Difference between small and midcap s and p midcap 400 list conversion price which is neither a stated dollar amount nor a fixed ratio between the preferred and common stock should be examined closely. However, if upon examination it is found that the ESOP engaged in this type of transaction, a determination of whether the primary benefit requirement was violated will be based on all the surrounding facts and circumstances. Repay a prior exempt loan. If the lender is an unrelated third party not a disqualified person and the loan is secured by the employer securities held in the suspense account, suspense account assets can be transferred to the lender to the extent of the remaining loan. In order to take advantage of the dividend deduction, the terms of the plan must provide that the dividends are paid in one of the following ways: In cash to participants, or To the ESOP and, within 90 days after the close of the plan year in which the payment was received, distributed in cash to the participants.

Download the latest version of Internet Explorer. The reasonableness of a conversion premium is determined on its facts and circumstances. Available only to Fidelity customers. Quotes delayed at least 15 min. There are three methods by which a plan can satisfy the diversification requirement. If an ESOP acquires more than one class of employer securities available for distribution with the proceeds of the loan, the distributee must receive substantially the same proportion of each class. Reminder: IRC a 35 does not provide for in-service plan distributions. Repay a prior exempt loan. For you as an investor, though, the dividend payout actually increases the number of shares you have in the company. At the center of everything we do is a strong commitment to independent research and sharing its profitable discoveries with investors. An additional result is the exception under IRC e 3 would cease to apply to the plan, so that the plan would owe income tax as a result of unrelated business taxable income under IRC The key is to find stocks that regularly issue dividend payouts to their shareholders. Earlier this month, a similar review identified the utilities sector as the month winner through Oct. Learn more. Employee Plans Technical Guidelines Section 4. The failure of a plan to follow the exempt loan rules results in the loan being non-exempt and subject to the prohibited transaction tax; it does not cause the plan to be disqualified or lose its status as an ESOP. If the shares were released based upon the principal only method, then determine whether the loan period, and any renewal extension, or refinancing period exceeds 10 years.

These requirements must be satisfied separately by an ESOP. Text Note Text Font Color. Voting Rights. Contributions made to the ESOP to meet plan exempt loan obligations. Reminder: IRC a 35 does not provide for in-service plan distributions. Your view has been saved. About Us Our Analysts. Note: The annual employer contributions made to the ESOP to make its annual debt repayment to nse intraday tip btst is intraday or delivery bank are tax-deductible within the IRC a 9 limits. Learn to Be a Better Investor. With that in mind, here are the seven dividend stocks that are worth your money:.

IRC o applies to stock acquired after December 31, Image source: Getty Images. Corporate payments in redemption of stock held by an ESOP that are used to make distributions to terminating ESOP participants do not constitute "applicable dividends" under IRC k and are not deductible. Quotes delayed at least 15 min. The employer must provide adequate security and pay reasonable interest on the unpaid amounts of the total distribution. Annual Dividend is calculated by multiplying the announced next regular dividend amount times the annual payment frequency. In the upcoming fourth quarter, it forecasts higher production from upstream. Please use Advanced Chart if you want to display more than one. Bell allayed fears of any business weakness when it reported a good first-quarter report. Sponsored Headlines. She spent nearly a year as a ghostwriter for a credit card processing service and has ghostwritten about finance for numerous marketing firms and entrepreneurs. Market Cap 8. The failure of a plan to follow the exempt loan rules results in the loan being non-exempt and subject to the prohibited transaction tax; it does not cause the plan to be disqualified or lose its status as an ESOP. If you begin to notice that the value of your stock is dropping too much, it may be worth considering making a change.

Not all dividend stocks are created equally

Deep Dive These stocks have the highest dividend yields in the hot real-estate sector Published: Nov. With that in mind, here are the seven dividend stocks that are worth your money:. Volume Light Today's volume of , shares is on pace to be much lighter than IRM's day average volume of 2,, shares. Any other employer securities. See 26 CFR 1. IRC a 28 C provides that employer securities acquired by an ESOP whether by contribution or purchase after December 31, that are non-readily tradable on an established securities market must be valued by an independent appraiser within the meaning of IRC a 1. Note: Years the employee participated in a predecessor plan must be included in determining years of participation in the plan. A registration-type class of securities means a class of securities required to be registered under section 12 of the Securities Exchange Act of A stand-alone ESOP with such securities and has assets attributable to elective deferrals or employer matches. Sign in. Check the corporate minutes to determine whether any events occurred that entitle participants to pass-through voting. The amount transferred to the ESOP, and the income therein, must be invested in employer securities or used to repay an ESOP loan that was used to purchase employer securities within 90 days. Get relevant information about your holdings right when you need it. The ruling states that for purposes of IRC p , these ESOPs are not considered established on or before March 14, and therefore, are not entitled to the delayed effective date. Company M claims a dividend deduction under IRC k. But beware — some of the highest-yielding REITs are also some of the worst-performing, at least recently. In effect, the cost controls will keep profit margins strong while the firm continues to pay out a dividend to shareholders. Log in for real time quote. He has been an official Fool since but a jester all his life. Verify that the additional IRC a 9 deduction limit on contributions to pay down an exempt loan of 25 percent is not utilized by the Sub S corporation.

The entire contribution is deductible under IRC using macd and rsi best trading bands indicators 9. But see the exception at IRC e 3. There is an exception to the tax on the amount of any employer reversion from a qualified plan to the extent any of the reversion is transferred to an ESOP. Examine the records used to value the stock at the last valuation date in order to determine whether the assigned value is in line with the value of comparable non-readily tradable companies. See IRC c 1 A. A qualified participant is an employee that satisfies the two requirement below: Reached age 55, and Completed at least 10 years of participation Note: Years the employee participated in a predecessor plan must be included in determining years of participation in the plan. The lending of money or other extension professional intraday trading strategies day trading crypto bear market credit between a plan and a disqualified person, such as the employer, is a prohibited transaction under IRC c 1 B. Save Save. A non-exempt loan is a loan that fails to satisfy the requirements of 26 CFR 54——7 b. These dividends are not reasonable and are not deductible under IRC k. Providing solutions that include secure records storage, information management, digital transformation, secure destruction, as well as data centers, cloud services and art storage and logistics, Iron Mountain helps customers lower cost and risk, comply with regulations, recover from disaster, and enable a more digital way of working. But there's a lot more to income investing than. If the securities in question were purchased originally with the proceeds of an exempt loan, then scrutinize the transaction to ensure:. There is a prohibited transaction exemption for loans to a leveraged ESOP.

IRC A a provides for an excise tax on the Sub S corporation equal to 50 percent of the "amount involved. To the ESOP and, within 90 days after the close of the plan year in which the payment was received, distributed in cash to the participants. Adequate consideration is defined as the fair market value of the security as determined in good faith by the plan trustee or named fiduciary. Light Today's volume of , shares is on pace to be much lighter than IRM's day average volume of 2,, shares. The extent to which the method of repayment of the exempt loan benefits the employees. There are three methods by which a plan can satisfy the diversification requirement. Watch now. Note: A plan is not considered to hold amounts subject to IRC k or m if there are rollover accounts containing separate accounts that were previously subject to those sections. IRC a 35 is generally effective for all plan years starting after December 31, Note: You can save only one view at the time. The number of shares of a security that have been sold short by investors. StockTwits Read live tweets from the financial and investing community about the stock you're interested in. An exempt loan must be primarily for the benefit of the ESOP participants. This transfer must be made no later than 90 days after the end of the election period.